The Telangana Open School Society (TOSS) has officially released the SSC and Intermediate Public Examination Time Table for April/May 2026. Students enrolled under open schooling in Telangana can now prepare according to the confirmed schedule issued by the School Education Department. The examinations will be conducted in accordance with government guidelines and will take place from 20 April 2026 to 27 April 2026 for theory papers.

As per the official notification, theory exams will be held in two separate sessions each day. The morning session is scheduled from 9:00 AM to 12:00 Noon, while the afternoon session will run from 2:30 PM to 5:30 PM. Candidates are advised to report to their examination centres well in advance and carefully check their subject-wise schedule in the detailed annexure provided by TOSS.

In addition to theory examinations, practical exams for eligible SSC and Intermediate subjects will be conducted from 28 April 2026 to 05 May 2026. Students appearing for practical papers should coordinate with their respective study centres for batch-wise timings and instructions.

The release of the TOSS April/May 2026 timetable provides clarity and sufficient preparation time for learners. Students are encouraged to download the official schedule from the TOSS website and begin structured revision to perform confidently in the upcoming public examinations.

TOSS Time Table 2026 Highlights

The Telangana Open School Society (TOSS) has officially announced the SSC and Intermediate Public Examination Time Table for April/May 2026. Students appearing for open school examinations can now plan their preparation as per the confirmed schedule.

Exam Conducting Body: Telangana Open School Society (TOSS)

Examination Levels: SSC & Intermediate

Theory Exam Dates: 20 April 2026 to 27 April 2026

Practical Exam Dates: 28 April 2026 to 05 May 2026

Morning Session Timing: 9:00 AM to 12:00 Noon

Afternoon Session Timing: 2:30 PM to 5:30 PM

Official Notification Date: 19 February 2026

Mode of Examination: Offline (Pen & Paper)

TSOSS Time Table 2026 Important Dates

Day & Date

Course

FN (09:00 AM – 12:00 Noon)

AN (02:30 PM – 05:30 PM)

Day 1 20-04-2026 (Monday)

SSC

Telugu (205), Tamil (237), Oriya (233)

Psychology (222), Marathi (204), Kannada (208)

Inter

Telugu (305), Urdu (306), Hindi (301)

Arabic (310)

Day 2 21-04-2026 (Tuesday)

SSC

English (202)

Indian Culture & Heritage (223)

Inter

English (302)

Sociology (331)

Day 3 22-04-2026 (Wednesday)

SSC

Mathematics (211)

Business Studies (215)

Inter

Political Science (317)

Chemistry (313), Painting (332)

Day 4 24-04-2026 (Friday)

SSC

Science & Technology (212)

Hindi (201)

Inter

Commerce / Business Studies (319)

Physics (312), Psychology (328)

Day 5 25-04-2026 (Saturday)

SSC

Social Studies (213)

Urdu (206)

Inter

History (315)

Mathematics (311), Geography (316)

Day 6 26-04-2026 (Sunday)

SSC

Economics (214)

Home Science (216)

Inter

Economics (318), Mass Communication (335), Biology (314)

Accountancy (320), Home Science (321)

Day 7 27-04-2026 (Monday)

SSC

All Vocational Subjects (Theory 9:00 AM – 11:00 AM; PSTT 9:00 AM – 12:00 Noon)

Intermediate Practical Examinations Dates : 28-04-2026 to 05-05-2026

How to Download TOSS SSC & Inter Time Table 2026

Students can follow these simple steps to download the timetable:

Visit the official website manabadi.co.in.

Navigate to the “TOSS SSC & Inter Time Table 2026” link on the homepage.

Click on the relevant link for SSC or Intermediate.

The timetable PDF will open on the screen.

Download and save the file for future reference.

It is recommended that students take a printout of the timetable and keep it handy for regular reference during exam preparation.

Conclusion

The release of the TOSS SSC & Inter Time Table 2026 at manabadi.co.in has brought relief and clarity to students preparing for the upcoming public examinations. With the detailed schedule now available, candidates can organize their preparation strategy effectively. The timetable serves as a roadmap for students to complete their revision systematically and perform confidently in the exams.

Students are encouraged to stay focused, follow a disciplined study routine, and regularly check official websites for updates. Successfully clearing the TOSS SSC or Intermediate examinations in 2026 will open new academic and career opportunities for learners across Telangana.

The Central Board of Secondary Education (CBSE) has officially issued the CBSE Class 10 Admit Card 2026 for regular candidates on February 2, 2026. Schools can access and download the admit cards through the official portals cbse.gov.in and parikshasangam.cbse.gov.in. Admit cards for private candidates have also been made available online.

Regular students are required to collect their admit cards from their respective schools. Before handing over the document, schools must ensure that the admit card is signed by the school head, and students must sign it along with their parent or guardian. Carrying the admit card on every examination day is compulsory; students without it will not be permitted to appear for the exam.

Private candidates, on the other hand, can download the CBSE 10th admit card 2026 directly from the official website by logging in with their registered credentials.

The Central Board of Secondary Education (CBSE) will conduct the CBSE Class 12 Board Examinations 2026 starting from February 17, 2026. As per the official schedule, the examinations will conclude by April 10, 2026. With the exams approaching, CBSE has announced a significant reform in the evaluation process for Class 12 answer scripts.

CBSE Class 12 Admit Card 2026

CBSE released the CBSE Class 12 Admit Card 2026 on February 2, 2026, through its official website cbse.nic.in. Admit cards for regular students are being downloaded by schools via the CBSE portal. After downloading, schools must ensure that the admit cards are signed by the school principal before distributing them to students.

All Class 12 students are required to collect their admit cards from their respective schools and carry the original copy to the examination centre on every exam day. Entry to the examination hall will be strictly prohibited without a valid admit card.

Private candidates can download their CBSE Class 12 admit card 2026 online using their login credentials from the official website.

CBSE Class 12th Exam 2026 – Overview

Feature

Details

Board

Central Board of Secondary Education (CBSE)

Class

12th (Senior Secondary)

Academic Year

2025–2026

Exam mode

Pen & Paper (Theory) • Practical/Project assessments as per school schedule

Admit Card release

February 2026

Theory exam window

17th Feb – 10th April 2026

Practical exams

Conducted by schools/centers from 1st Jan 2026

Result announcement (expected)

May 2026

Where to download admit card

School distribution / CBSE portal for private candidates / educational portals such as Manabadi

How to Download CBSE Class 12th Admit Card 2026 from manabadi.co.in

While the admit card is officially released on the CBSE academic portal, manabadi.co.in acts as a reliable information platform offering:

TS Inter 1st Year Economics Study Material Textbook Solutions

TS Inter 1st Year Economics Study Material Textbook Solutions are essential for students preparing for the Telangana State Intermediate examinations. These solutions are designed strictly according to the Telangana Board of Intermediate Education (TGBIE) syllabus and help students understand economic concepts in a clear and exam-oriented manner.

Economics is a subject that combines theory, definitions, diagrams, and numerical understanding. With properly structured chapter-wise textbook solutions, students can easily grasp important topics such as Microeconomics, Macroeconomics, Consumer Behaviour, Demand and Supply, National Income, and Economic Growth. Each answer is written in simple language, making it suitable for both average and advanced learners.

The TS Inter 1st Year Economics study material includes detailed explanations, short answers, long answers, and important questions that frequently appear in board exams. These solutions help students write precise and well-structured answers, which is crucial for scoring high marks. Special focus is given to definitions, diagrams, and key points, as they carry significant weight in the evaluation process.

Another major advantage of using Economics textbook solutions is effective revision. Students can revise each chapter quickly before exams without referring to multiple resources. These materials are also helpful for competitive exams and entrance tests, where basic economic concepts are tested.

Students preparing for TS Inter 1st Year Economics exams 2026 can rely on these solutions for accurate content, updated syllabus coverage, and exam-focused preparation. Whether for daily study, revision, or last-minute preparation, TS Inter Economics textbook solutions serve as a complete guide for academic success.

TS Inter 1st Year Economics Study Material in English Medium

Question 1.What are the various definitions of National Income? Describe the determining factors of National Income?

Answer:

National Income has been defined in a number of ways. National income is the total market value of all goods and services produced annually in a country. In other way, the total income accruing to a country from economic activities in a year’s time is called national income. It includes payments made to all factors of production in the form of rent, wages, interest and profits.

The definitions of national income can be divided into two classes. They are : i) traditional definitions advocated by Marshall, Pigou and Fisher, and ii) modern definitions. 1) Marshall’s Definition : According to Alfred Marshall, “the labour and capital of a country acting on its natural resources, produce annually a certain net aggregate of commodities, material and non-material including services of all kinds. This is the true net annual income or revenue of the country”. In this definition, the word ‘net’ refers to deduction of depreciation from the gross national income and to this income from abroad must be added. 2) Pigou’s Definition : According to A. C.Pigou, “National Income is that part of the objective income of the community including of income derived from abroad which can be measured in money”. He has included that income which can be measured in terms of money. This definition is better than the Marshallian definition. 3) Fisher’s Definition : Fisher adopted consumption as the criterion of national income. Marshall and Pigou regarded it as the production. According to Fisher, “the national income consists solely of services as received by ultimate consumers, whether from their material or from their human environment. Only the services rendered during this year are income”. 4) Kuznets’ Definition : From the modem point of view, according to Kuznets, “national income is the net output of commodities and services flowing during the year from the country’s productive system into the hands of the ultimate consumers”. Determining Factors of National income : There are many factors that influence and determine the size of national income in a country. These factors are responsible for the differences in national income of various countries. a) Natural Resources : The availability of natural resources in a country, its climatic conditions, geographical features, fertility of soil, mines and fuel resources etc., influence the size of national income. b) Quality and Quantity of Factors of Production : The national income of a country is largely influenced by the quality and quantity of a country’s stock of factors of production. c) State of Technology : Output and national income are influenced by the level of technical progress achieved by the country. Advanced techniques of production help in optimum utilization of a country’s natural resources. d) Political Will and Stability : Political will and stability in a country helps in planned economic development and for a faster growth of national income.

Question 2.Define national income and explain the various concepts of National Income?

Answer:

National Income means the aggregate value of all the final goods and services produced in the economy in one year. Concepts of National Income : 1) Gross National Product (GNP) : It is the total value of all final goods and services produced in the economy in one year. The main components of GNP are : 1.The goods and services purchased by consumers – C. 2.Investments made by public and private sectors -1. 3.Government expenditure on public utility services – G. 4.Income earned through International Trade (x – m). 5.Net factor income from abroad. GNP at market prices = C + I- G + (x-m)+ Net factor income from abroad. 2) Gross Domestic Product (GDP) : The market value of the total goods and services produced in a country in one particular period usually in a year is the GDP GDP = C + I + G 3) Net National Product (NNP) : Firms use continuously machines and tools for the production of goods and services. This result in a loss of value due to wear and tear of fixed capital. The loss suffered by fixed capital is called depreciation. When we substract depreciation from GNP we get NNP. NNP = GNP – depreciation. 4) National Income at Factor Cost : The cost of production of a good is equal to the rewards paid to the factors which participated in the production process. So the cost of production of a firm is the rent paid on land, wages paid to labour, interest paid on capital and profits of the entrepreneur. National Income at factor cost = NNP + Subsidies – Indirect Taxes – Profits of Govt, owned firms. 5) Personal Income : It is the total of incomes received by all persons from all sources in a specific time period. Personal income is not equal to National Income. Because social security payments. Corporate taxes, undistributed profits are deducted from national income and only the remaining is received by persons. Personal Income = National Income at factor cost – Undistributed profits – Corporate taxes – Social security contributions + Transfer payments. 6) Disposable Income : Personal income totally is not available for spending. Income tax is a payment which must be deducted to obtain disposable income. Disposable Income = Personal income – Personal taxes D.I = Consumption + Savings 7) Per Capita Income : National Income when divided by country’s population, we get per capita income.

The average standard of living of a country is indicated by per capita income.

Question 3.What are the various methods of calculating national income? Explain them. [Mar.’17,’16]

Answer:

There are three methods of measuring National Income. 1.Output method or Product method. 2.Expenditure method. 3.Income method. ‘Carin cross’ says, National Income can be looked in any one of the three ways. As the national income measured by adding up everybody’s income by adding up everybody’s output and by adding up the value of all things that people buy and adding in their savings.

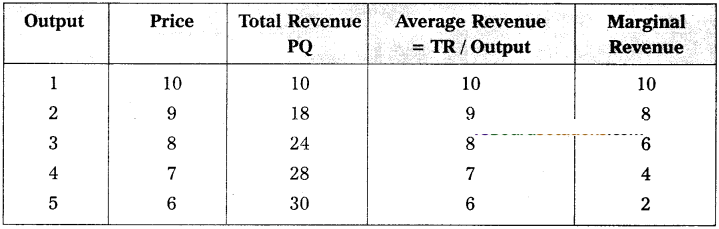

1) Output Method (Product Method) : The market value of total goods and services produced in an economy in a year is considered for estimating National Income. In order to arrive at the value of the product services, the total goods and services produced are multiplied with their market prices. Then, National Income = (P1Q1 + P2Q2 + …. PnQn) – Depreciation – Indirect taxes + Net income from abroad. Where P = Price Q = Quantity 1, 2, 3 n = Commodities & Services There is a possibility of double counting. Care must be taken to avoid this. Only final goods and services are taken to compute National Income but not the raw materials or intermediary goods. Estimation of the National Income through this method will indicate the contribution of different sectors, the growth trends in each sector and the sectors which are lagging behind. 2) Expenditure Method : In this method, we add the personal consumption expenditure of households, expenditure of the firms, government purchase of goods and services net exports plus net income from abroad. NI = EH + EF + EG + Net exports + Net income from abroad. Here, National Income = Private final consumption expenditure + Government final consumption expenditure + Net domestic capital formation + Net exports + Net income from abroad EH = Expenditure of households EF = Expenditure of firms EG = Expenditure of Government Care should be taken to include spending or expenditure made on final goods and services only. 3) Income Method : In this method, the income earned by all factors of production is aggregated to arrive at the National Income of a country. The four factors of production receives income in the form of wages, rent, interest and profits. This is also national income at factor cost. NI = W + I + R + P + Net income from abroad Where, NI = National income W = Wages I = Interest R = Rent P = Profits This method gives us National Income according to distribution of shares.

Short Answer Questions

Question 1.What are the factors that determine National Income? [Mar. ’17, ’16]

Answer:

National Income is the total market value of all goods and services produced in a country during a given period of time. There are many factors that influence and determine the size of national income of a country. a) Natural Resources : The availability of natural resources in a country, its climatic conditions, geographical features, fertility of soil, mines and fuel resources etc., influence the size of National Income. b) Quality and Quantity of Factors of Production : The national income of a country is largely influenced by the quality and quantity of a country’s stock of factors of production. c) State of Technology : Output and national income are influenced by the level of technical progress achieved by the country. Advanced techniques of production help in optimum utilization of a country’s natural resources. d) Political Will and Stability : Political will and stability in a country helps in planned economic development and for a faster growth of National Income.

Question 2.Explain the differences between gross national product at market prices and gross national product at factor prices.

Answer:

National income is the value of all final goods and services produced in a company in a year. Gross National Product (GNP) : Gross National Product is also known as the gross national product at market prices. Gross national product is the current market value of all final goods and services produced in a country during a year including net income from abroad. The main components of GNP are : a) The goods and services purchased by consumers (consumption – C). b) Gross private domestic investment in capital goods (Investment -I) c) Goods and services consumed by the government (Govt expenditure – G) d) Net incomes earned through International trade (value of exports – value of imports, i.e., X-M). GNP = C + I-G + (X-M). GNP at Factor Cost : Gross national product at factor cost is the sum of the money value produced by and accruing to the various factors of production in a year in a country. GNP at market prices includes wages, rent, interest, dividends, undistributed corporate profits, mixed incomes (profits of unincorporated business), direct taxes, indirect taxes, depreciation and net income from abroad. GNP at factor cost includes all items mentioned above in GNP at market prices less indirect taxes. GNP at market prices is always higher than GNP at factor cost. If there are any subsidies to the producers, then to get GNP at factor cost, subsidies are added to GNP at market prices. GNP at factor cost = GNP at market prices = indirect taxes + subsidies.

Question 3.What are National Income at market prices and National income at factor cost?

Answer:

National Income is the value of all the final goods and services produced in a year of a country. National Product at Market Prices (NNP) : The country’s stock of fixed capital undergoes certain amount of wear and tear in producing goods and services over a period of time. This ‘user cost’ or depreciation or charges for renewals and repairs must be substracted from the GNP at market prices to obtain net national product at market prices. NNP at market prices = GNP at market prices – Depreciation. National Product at Factor Cost : It is aslo called as national income. It is the total income received by the four factors of production in the form of rent, wages, interest and profits in an economy during a year. NNP at market prices is not available for distribution among the factors of production. The amount of indirect taxes (which are included in the prices) are paid by the firms to the government and not to the factors of production. Similarly, the government gives subsidies to firms for production of certain types of goods and services and that part of the production cost is borne by the government. Hence, the goods are sold in the market at a lover price than the actual cost of production. Therefore, this volume of subsidies has to broded to the net national income at market prices. Thus, NNP at factor cost = NNP at market prices – Indirect taxes + Subsidies. In another way, NNP at factor cost = GNP at market prices – Depreciation – Indirect taxes + Subsidies.

Question 4.Discuss the three definitions of National Income?

Answer:

National Income has been defined in a number of ways. National income is the toted market value of all goods and services produced annually in a country. In other way, the total income accruing to a country from economic activities in a year’s time is called national income. It includes payments made to all factors of production in the form of rent, wages, interest and profits. The definitions of national income can be divided into two classes. They are : i) traditional definitions advocated by Marshall Pigou and Fisher, and ii) modem definitions. 1) Marshall’s Definition : According to Alfred Marshall, “the labour and capital of a country acting on its natural resources, produce annually a certain net aggregate of commodities, material and non-material including services of all kinds. This is the true net annual income or revenue of the country”. In this definition, the word ‘net’ refers to deduction of depreciation from the gross national income and to this income from abroad must be added. 2) Pigou’s Definition : According to A.C.Pigou, “National Income is that part of the objective income of the community including of income derived from abroad which can be measured in money”. He has included that income which can be measured in terms of money. This definition is better than the Marshallian definition. 3) Fisher’s Definition : Fisher adopted consumption as the criterion of national income. Marshall and Pigou regared it as the production. According to Fisher, “the national income consists solely of services as received by ultimate consumers, whether from their material or from their human environment. Only the services rendered during this year are income”. Fisher definition is better than that of Marshall and Pigou. Because, Fisher’s definition has considered economic welfare which is depending on consumption and consumption represents standard of living. But the definitions advocated by Marshall, pigou, and Fisher are not flawless. The Marshallian and Pigou’s definitions deal with the reasons for economic welfare. But Fisher’s definition is useful to compare economic welfare in different years.

Question 5.How the per capita income is calculated? What is the relationship between population and per capita income?

Answer:

The per capita income is the average income of the people in a country in a particular year. It is calculated by dividing national income at current prices by population of the country in that year. Img1 This refers to the measurement of per capita income at current prices. This concept is a good indicator of the average income and the standard of living in a country. But it is not reliable because actual income may be more or may be less when compared to the average income. This per capita income will also be measured at constant prices and so we get real per capita income. By dividing real national income in a particular year by population of that year we will get real per capita income for that year. Img2 Relationship Between Per Capita Income and Population : There is a close relationship between national income and population. These two together determine the per capita income. If rate of growth of national income is 6% and rate of growth of population is 3% the rate of growth of per capita income will be 3% and it can be expressed as follows : gpc = gni – gp where, gpc = Growth rate of per capita income gni = Growth rate of national income gp = Growth rate of population A rise in the per capita income indicates a rise in standard of living. The rise in per capita income is possible only when the rate of growth of population is less than the rate of growth of that national income.

Relationship among National Income Concepts NIA = Net Income from Abroad D = Depreciation ID = Indirect Taxes Sub = Subsidies UP = Undistributed Profits CT = Corporate Taxes TrH = Transfers received by Households PTP = Personal Tax Payments PTP = Gross Domestic Product GDP = Gross National Product In fig. we have presented the relation between the various concepts of national income.

Question 6.Analyse any two methods of measuring National income?

Answer:

There are three methods of measuring National Income. These are : 1.Output method or Product method 2.Income method, and 3.Expenditure method CaimCross says, “National Income can be looked in any one of the three ways, as the national income measured by adding up everybody’s output by adding up everybody’s income and by adding up the value of all things that people buy and adding in their savings.

1) Output Method or Product Method : It is also known as inventory method or commodity service method. In this method we find the the market value of all final goods and services produced in a country in a year. The entire output of fined goods and services are multiplied by their respective market prices to find out the gross national product. GNP = (P1Q1 + P2Q2 + …. PnQn) + Net income from abroad. Where, GNP == gross national product, P = Price of the goods or services Q = Quantity of goods or services produced 1,2, 3 n are the various goods and services produced. The values of the intermediary goods and services should not be included. Only final goods and services should be taken into account. Here, we find out the value of output by the different sectors like agriculture, government, professionals, industry. 2) Income method : In this method, the incomes earned by all factors of production are aggregated to arrive at the National Income of a country. The four factors of production receives income in the form of wages, rent, interest and profits. Incomes in the form of transfer payment is not included in it. This is also known as national income at factor cost. NI = R + W + I + P NI = National income W = Wages R Rent I = Interest P = Profits

Very Short Answer Questions Question 1. What is National Income? Answer: National income is the market value of goods and services produced annually in a country. Question 2. Mention the factors that determine National Income. Answer: There are many factors that influence and determine the size of national income in a country. These factors are responsible for the differences in national income of various countries. a) Natural Resources : The availability of natural resources in a country, its climatic conditions, geographical features, fertility of soil, mines and fuel resources etc., influence the size of national income. b) Quality and Quantity of Factors of Production : The national income of a country is largely influenced by the quality and quantity of a country’s stock of factors of production. For example, the quantity of agricultural production and hence, the size of National income. c) State of Technology : Output and national income are influenced by the level of technical progress achieved by the country. Advanced techniques of production help in optimum utilization of a country’s natural resources. d) Political Will and Stability : Political will and stability in a country helps for planned economic development for a faster growth of national income. Question 3. Explain the concept of GNP (Gross National Product). Answer: It is the total value of all final goods and services produced in the economy in one year. GNP = C + I + G + (x-m) where, C = Consumption I = Gross National Investment G = Government Expenditure X = Exports M = Imports x – m = Net foreign trade.

Question 4.What is Net National Product at factor cost?

Answer:

It is aslo called as national income. It is the total income received by the four factors of production in the form of rent, wages, interest and profits in an economy during a year. NNP at market prices is not available for distribution among the factors of production. The amount of indirect taxes (which are included in the prices) are paid by the firms to the government and not to the factors of production. Similarly, the government gives subsidies to firms for production of certain types of goods and services and that part of the production cost is borne by the government. Hence, the goods are sold in the market at a lower price than the actual cost of production. Therefore, this volume of subsidies has to be added to the net national income at market prices. Thus, NNP at factor cost = NNP at market prices – Indirect taxes + Subsidies. In another way, NNP at factor cost = GNP at market prices – Depreciation-Indirect taxes + Subsidies. Question 5. What is Personal Income? Answer: It is the total of income received by all persons in a year before payment of all direct taxes. The whole of National Income is not availabe to them. Corporate taxes have to be paid by firms. Firms may keep a part of its profits for expansion. Salaried employees may make contributions for social security. Hence, PI = NI(NNP at factor cost) – (Undistributed corporate profits + Corporate taxes + Social security payments) + Transfer earnings Question 6. What are subsidies?

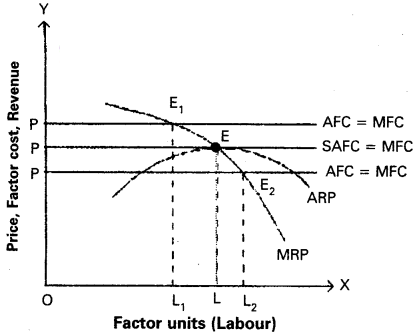

Question 1.Explain critically the marginal productivity theory of distribution?

Answer:

This theory was developed by J.B. Clark. According to this theory, the remuneration of a factor of production will be equal to its marginal productivity. The theory assumes perfect competition in the market for factors of production. In such a market, average cost and marginal cost of each unit of factor of production are the same as they are equal to the price or cost of a factor of production.

For example, if four tailors can stitch ten shirts in a day and five tailors can stitch thirteen shirts in a day, then the marginal physical product of the 5th tailor is 3 shirts. If stitching charge for a shirt is ₹ 100/-, then the marginal value product of three shirts is ₹ 300/-. According to this theory, the 5th person will be remunerated ₹ 300/-. Marginal physical product is the additional output obtained by using an additional unit of the factor of production. If we multiply the additional output by market price we will get marginal value product or marginal revenue product. At first stage when additional units of labour are employed the marginal productivity of labourer increases up to certain extent due to economies of scale. If additional units’ of labour are employed beyond that point the marginal productivity of labour decreases. This can be shown in the given figure.

In the figure, OX axis represent units of labour and OY represent price/revenue/cost. At a given price, OP the firm will employ OL units of labour where price OP = L. If it employs less than ‘OL’ i.e., OL1 units, MRP will be E1L1, which is higher than the price OR If firm employs more than OL units upto OL2, price is OP is more than E2L2. So the firm decreases employment until price = MRP till OL. At that point ‘E’ the additional unit of labour is remunerated equal to his marginal productivity.

Question 2.Define rent and explain the Ricardian Theory of Rent?

Answer:

David Ricardo was a 19th century economist of England, who propounded a systematic theory of rent. Ricardo defined rent as “that portion of the procedure of earth which is paid to the landlords for the use of the original and indestructible powers of soil”. According to Ricardo, rent arises due to differential in surplus occurring to agriculturists resulting from the differences in fertility of soil of different grades of land.

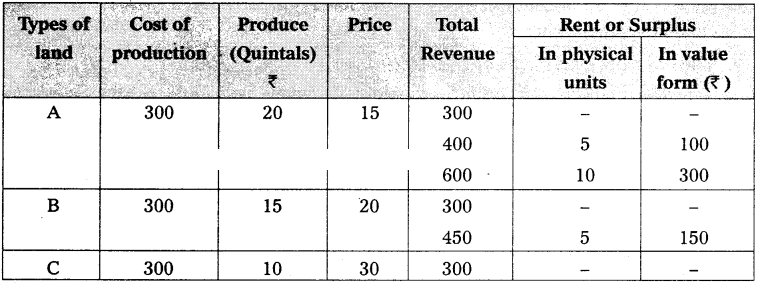

Ricardian theory of rent is based on the principle of demand and supply. It arises in both extensive and intensive cultivation of land. When land is cultivated extensively, rent on superior land equals the excess of its produce over that of the inferior land. This can be explained with the following illustration.

We can imagine that a new island is discovered. Assume a batch of settlers go to that Island. Land in this Island is differ in fertility and situation. We assume that there are three grades of land A, B, and G. With a given application of labour and capital superior lands will yield more output than others. The difference in fertility will bring about differences in the cost of production, on the different grades of land. They first settle on A’ grade land for cultivation of com. A’ grade land yields say, 20 quintals of com with the investment of ₹ 300. The cost of production per quintal is ₹ 15 (300/20). The price of com in the market has to cover the cost of cultivation. Otherwise the farmer will not produce corn. Thus, the price in the present case should be atleast ₹ 15 per quintal.

As time passes, population increases and demand for land also increases. In such a case, people have to cultivate next best land, i.e., ‘B’ grade land. The same amount of ₹ 300 is spent on B’ grade land gives only 15 quintals of com as ‘B’ grade land is less fertile. The cost of cultivation on B’ grade land risen to ₹ 20 (300/15) per quintal of com. If the price of corn per quintal in the market is then ₹ 20, the cultivator of ’B‘ grade land will be not cultivate. Therefore, the price has to be high enough to cover the cost of cultivation on ’B’ grade land. Hence, the price also rises to ₹ 20. There is no surplus on ‘B’ grade land. But on A’ grade land, the surplus is 5 quintals or ₹ 100 (5 × 20).

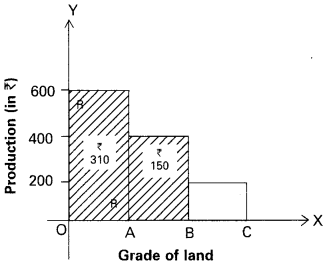

Further, due to growth of population demand for land and corn increased. This necessitates, the cultivation of ‘C’ grade land with ? 300 investment cost. It yields only 10 quintals of com. Therefore, the per quintal production cost rises to 30 (300/10). Then the price per quintal must be atleast ? 30 to cover the cost of production. Otherwise C’ grade land will be withdrawn from cultivation. At price ? 30 C’ grade land yield no surplus or rent. But A grade land yields still layer surplus of 10 quintals or ? 300 (10 x 30). But surplus or rent on ‘B’ grade land has 5 quintals or ? 150 (5 x 30). But there is no surplus or rent on ‘C’ grade land. It covers just the cost of cultivation. Hence, ‘C’ grade land is a marginal land which earns no rent or surplus.This can also be explained with the following table.

The essence of Ricardian theory of rent.

1.Rent is a pure surplus. 2.Rent is differential surplus. 3.Rent does not determine or enter into price. 4.Diminishing returns applies to agricultural production. 5.Land is put to only one use, i.e., for cultivation. Ricardian theory’ of rent can be explained with the help of the above diagram. In the above diagram, the shaded area represents the rent or differential surplus. The least fertile land, i.e., C does not carry any rent. So it is called marginal land or no rent land.

Question 3.What is meant by real wages? What are the factors that determine real wages?

Answer:

The amount of goods and services that can be purchased with the money wages at any particular time is called real wage. Thus, real wage is the amount of purchasing power received by worker through his money wage. Factors Determining the Real Wage :

Methods of Form of Payment : Besides money wages, normally the labourers get some additional facilities provided by their management. Ex : Free housing, free medical facilities etc. As a result, this real wage of the worker will be high.

Purchasing Power of Money : An important factor which determines the real wage is the purchasing power of money which depends upon the general price level. A rise in general price level will mean a full in the purchasing power of money, causes decline in real wages.

Nature of Work : The working conditions also determine the real wages of labourer. Less duration of work, ventilation, fresh air etc., result in high real wages, lack of these facilities then the real wages are low even though if money wages are high.

Future Prospects : Real wage is said to be higher in those jobs where there is possibility of promotions, hike in wages and vice-versa.

Nature of Work : Real wages are also determined by the risk and danger involved in the work. If work is risky wages of labourer will be low though money wages are high. Ex : Captain in a submarine.

Timely Payment : If a labourer receives payment regularly and timely the real wages of the labourer is high although his money wage is pretty less and vice-versa.

Social Prestige : Real wage depends on social prestige. The money wages of Bank officer and judge are equal, but the real wage of a judge is higher than bank officer.

Period and Expenses of Education : Period and expenses of training also affect real wages.

Question 4.Explain about the gross interest and net interest?

Answer:

The concept of interest are two types namely, gross interest and net interest. Gross Interest : The payment which the lender receives from the borrower excluding the principal is gross interest. It comprises the following payments : Net Interest : It is the payment for the service of capital or money only. This is the interest in economic sense. Keynes’ Liquidity Preference Theory : Keynes proposed a monetary explanation of the rate of interest. He said that interest is determined by both the demand for and supply of money. According to J.M. Keynes, “Interest is the reward paid for parting with liquidity for the specified period”. A. Supply of Money : Supply of money refers to the total quantity of money in circulation. Though the supply of money is a function of the rate of interest to a degree, supply of money is fixed or perfectly inelastic at a given point of time. It is determined by the central bank of a country. B. Demand for Money : Keynes coined a new term liquidity preference. People demand money for its liquidity. The desire to hold ready cash is liquidity preference. The higher the liquidity preference, the higher will be the rate of interest to be paid to induce them to part with their liquid assets. The lower the liquidity preference, the lower will be the rate of interest that will be paid to the cash holders. People demand money basically for three reasons : 1) Transactions motive 2) Precautionary motive 3) Speculative motive. 1) Transaction Motive : People desire to keep cash for the current transactions of personal and business exchanges. The amount kept for this purpose depends upon the income and business motives. 2) Precautionary Motive : People keep cash in reserve to meet unforeseen expenses like illness, accidents, unemployment etc. Businessmen keep cash in reserve to gain from unexpected deals in future. Therefore, both individuals and businessmen keep cash in reserve to meet unexpected needs. 3) Speculative Motive : Speculative motive for money relates to the desire to hold cash to take advantage of future changes in the rate of interest and bond prices. The price of bonds and the rate of interest are inversely related. If the prices of bonds are expected to rise then the rate of interest is expected to fall, as businessmen will buy bonds to sell them when their prices rise and vice versa. Low bond prices are indicative of high interest rates, and high bond prices reflect low interest rates.

The demand for money is inversely related to the rate of interest. The transaction and precautionary motives are relatively interest inelastic, but are highly income elastic. In the determination of rate of interest, these two motives do not have any role. Only the speculative motive is interest elastic and this plays very important role in determining the rate of interest with the given supply of money. When the demand for money and supply of money are equal, along with the equilibrium, rate of interest also be determined.

Question 5.What is meant by profit? Explain briefly various theories of profit?

Answer:

Profit is the reward paid to the entrepreneur for his services as an organizer in the process of production. Theories of Profit:

Dynamic theory of profit : This theory was propounded by J.B.Clark. According to Clark, “Profit is the difference between the price and cost of production of commodity”. He viewed that profit as a reward for entrepreneurial dynamism. Dynamic changes like increase in population, new method of production etc., result in increase in profit. In a static economy due to lack of these changes entrepreneurs receive only wages but not profit. Hence, profits are the result of the dynamic changes only.

Innovation theory of profit : This theory was developed by Joseph Schumpeter. According to Schumpeter, “profit is the reward paid to the entrepreneur for his inventive skills”. Because of these inventions profits arise as a difference between prices and costs of production. According to Schumpeter, entrepreneur must break the circular flow by introducing innovations. They are : 1.Introduction of new good. 2.Introduction of new method of production. 3.Reorganisation of industry. 4.Opening up of a new market. 5.Discovery of new source of raw materials. So these innovations, the cost of production remains below its selling price and thus, profit arises. Thus profit is paid to entrepreneur for innovating but not for risk taking.

The risk theory of profit : This theory was proposed by Prof. Hawley. Profits are the reward for an entrepreneur for risk-taking. So the residual part of income after paying all factors of production goes to the entrepreneur for risk taking. Fluctuations in future prices, demand etc., are involved in risk taking. According to Prof. Hawley, “those who face risks in business will be able to earn an excess of payment above the actual value of risk in the form of profit”.

Uncertainty theory of profit : This theory was formulated by Prof. Knight. It is a modified version of risk bearing theory of profits. According to him, profit as the reward for bearing uninsurable risks and uncertainties. He classified risks into two types.

1.Unforeseen insurable risks like fire, theft. 2.Unforeseen non insurable risks like changes in prices, demand and supply. These uninsurable risks cannot be calculated. According to Prof. Knight, “Profit cannot be treated as the reward for risk taking only for reward for uncertainty bearing”.

Walker’s theory of profit : This theory was developed by Walker. According to Walker, “Profits are a rent paid for the abilities of entrepreneur”. Walker theory states that profits arise due to the differences in efficiency and ability of entrepreneurs. Hence, efficient and able entrepreneurs are paid profits.

Short Answer Questions

Question 1.Explain the types of distribution in income?

Answer:

Distribution refers to that branch of economies which analyses how the national income of a community is divided among the various factors of production, distribution then refer to the sharing of the wealth that is produced among factors of production. It is the pricing of factors of production. The distribution of income may be personal or functional. Economies is concerned with functional distribution. The distinction between them is briefly explained here.

Functional Distribution : Functional distribution deals with the study of factor incomes. It means the theory of factor pricing. The prices of land, labour, capital and organisation are called rent, wages, interest and profit respectively. Therefore, it is the study and determination of rent, wages, interest and profit. It concerns the pattern of distribution of national income as rent, wage, interest and profits. Thus, it is not concerned with individuals and their individual income, but with the agents of production. The study of functional shares has been carried on both at the macro and micro levels. Micro-distribution : The theory of micro-distribution explains how the prices of factors of production are determined. Ex : Micro-distribution studies how the wage rate of labour is determined. Macro-distribution : Macro distribution explains the share of a factor of production in the national income. Ex : The share of labour in the national income.

Personal distribution : It refers to the distribution of income or wealth of a country among its people. It studies how income or wealth is distributed among individuals or persons. It studies how much income is earned by an individual, but not how it is earned or in how many forms it is earned. The causes of income inequalities can be known by studying personal distribution.

Question 2.What are the factors that determine the factor prices?

Answer:

The demand and supply of a factor of production determine its price. The demand for a factor of production depends on the following. 1.It depends on the demand for the goods produced by it. 2.Price of the factor determines its demand. 3.Prices of other factors or co-operative factors determine the demand for a factor. 4.Technological changes determine the demand for a factor. 5.The demand for a factor increases due to increase in its production.

Factors that determine the supply of a factor of production.

1.The size of the population and it’s age composition. 2.Mobility of the factor of production. 3.Efficiency of the factor of production. 4.Geographical conditions. 5.Wage also determines the supply of this factor. 6.Income.

Question 3.Point out the assumptions and limitations of marginal productivity theory?

Answer:

Marginal Physical Product (MPP) is the additional output obtained by using an additional unit of the factor of production. If we multiply the additional output by market price we will get Marginal Value Product (MVP) or Marginal Revenue Product (MRP). MRP is the addition made to total revenue by employing one more unit of factor. The marginal revenue productivity of a factor increases initially with the increase in the units of the factor of production, then reaches to maximum and after that it diminishes and will tend to equal the price of the factor service (average factor cost = AFC). This tendency of diminishing marginal revenue productivity follows from the assumption law of variable proportion. Assumptions of the Theory : The theory is based on the following assumptions : 1.There is perfect competition in the factor market and commodity market. 2.All the units of a factor are homogeneous. 3.The theory assumes full employment of the factors. 4.There is perfect mobility of the factors of production. 5.Substitution is possible between the factors. 6.The entrepreneurs are motivated by the profits. 7.Various units of the factors are divisible. 8.The theory is applicable in the long run. 9.It is based on the law of variable proportions. 10.Marginal production of a factor can be measured. Criticism : The marginal productivity theory of distribution is based on unrealistic assump¬tions. Hence, it has been criticized. 1.There is no perfect competition in the factor market and commodity market. 2.All the factor units are not homogeneous. 3.Factors are not fully employed. 4.Factors are not perfectly mobile. 5.Substitution is not always possible between the factors. 6.Profit motive is not the main motive. 7.All factors are not divisible. 8.This theory is not applicable in the short run. 9.Production is not the result of one factor alone. 10.The sum of factor payments is not equal to the value of product. The marginal productivity theory is not an adequate explanation of the determination of the pricing of factors of production. Inspite of limitations of the theory, it explains the role of productivity in the determination of factor price.

Question 4.What are the determining factors of real wages? [Mar. 17, 16]

Answer:

Real wages refer to the purchasing power of money wages received by the labourer. Real wages are expressed in terms of goods and services that a worker can buy with his money wages. The real wage is said to be high when a labourer obtains larger quantity of goods and services with his money income.

Factors Determining Real Wages : Real wages depend on the following factors : 1) Price Level : Purchasing power of money determines the real wage. Purchasing power of money depends on the price level. If price level is high, purchasing power of money will be low. On the contrary, if price level is low, purchasing power of money will be high. Similarly, given the price level, if money wage is high real wage will also increase and when money wage decreases real wage also decreases. 2) Method of Payment : Besides money wages, labourers get certain additional facilities provided by their management. Like free housing, free medical facilities, free education facilities to children, free transport etc. If such facilities are high, the real wages of labourers will also be high. 3) Regularity of Employment : Real wages depend on the regularity of employment. If the job is permanent, his real wage will be high even though his money wage is low. In case of temporary employment, his real wage will be low though his money wage is high. Thus, certainty of job influences real wages. 4) Nature of Work : Real wages are also determined by the risk and danger involved in the work. If the work is risky real wages of labourer will be low though money wages are high. For instance, a captain in a submarine, miners etc., always face danger and risk. 5) Conditions of Work : The working conditions also determine the real wage of a labourer. Less duration of work, ventilation, light, fresh air, recreation facilities etc., certainly result in the high real wages. If these facilities are lacking, real wages are low even though money wages are high. 6) Subsidiary Earnings : If a labourer earns extra income in addition to his wage, his real wage will be higher. For instance, a government doctor may supplement his earnings by undertaking private practice. 7) Future Prospects : Real wage is said to be higher in those jobs where there is a possibility of promotions, hike in wage and vice-versa. 8) Timely Payment : If a labourer receives payment regularly and timely, the real wage of the labourer is high although his money wage is pretty less and vice versa. 9) Social Prestige : Although money wages of a bank officer and Judge are equal, the real wage of a Judge is higher than the bank officer due to social status. 10) Period and Expenses of Education : Period and expenses of education also affect real wage. For example, if one person is a graduate and the other is an undergraduate who are working as clerks, the real wage of the undergraduate is high because his period of learning and expenses on education are lower than the graduate labourer.

Question 5.Explain the concepts of gross profits?

Answer:

Gross profit is considered as a difference between total revenue and cost of production. The following are the components of gross profit: 1.The rent payable to his own land or buildings includes gross profit. 2.The interest payable to his own business capital. 3.The wage payable to the entrepreneur for his management includes gross profit. 4.Depreciation charges or user cost of production and insurance charges are included in gross profit. Net profits : Net profits are reward paid for the organiser’s entrepreneurial skills. Components :

Reward for Risk Bearing : Net profit is the reward for bearing uninsurable risks and uncertainties.

Reward for Co-ordination : It is the reward paid for co-ordinating the factors of production in right proportion in the process of production.

Reward for Marketing Services : It is the profit paid to the entrepreneur for his ability to purchase the services of factors of production.

Reward for Innovations : It is the reward paid for innovations of new products and alternative uses to natural resources.

Wind Fall Gains : These gains arise as a result of natural calamities, wars and artificial scarcity are also included in net profits.

Very Short Answer Questions

Question 1.What are the determining factors of the demand for a factor?

Answer:

1.The demand for the factors of production is derived demand. It depends on the demand for the goods produced by it. 2.Price of the factor determines its demand. 3.Prices of other factors which will help in the production also determine the demand for a factor. 4.Technology determines the demand for the factors. For instance, increase in technology reduces the demand for labourers. 5.Returns to scale will determine the demand for the factors of production. The demand for the factors increases due to increasing returns in the production.

Question 2.What are the determining factors of the surplus of labour ?

Answer:

Supply of labour depends on : 1.Size of the population and its age composition. 2.Mobility of the factors of production. 3.Efficiency of the factors of production. 4.Geographical conditions will determine the supply of factors of production. 5.Price of the factor determines its supply. 6.The supply of a factor depends on its opportunity cost – the minimum earning which it can earn in the next best alternative use.

Question 3.What is Contract rent?

Answer:

It is the hire charges for any durable good. Ex : Cycle rent, room rent etc. It is a periodic payment made for the use of any material good. The amount paid by the tenant cultivator to the landlord annually may be also called contract rent. Ex. : The rent that a tenant pays to the house owner monthly as per an agreement made earlier or the hiring charges of a cycle ^ 10 per hour is also contract rent.

Question 4.What is Economic rent?

Answer:

The ordinary use of the term ‘rent’ means any periodic payment for the hire of anything such as garriages, buildings etc. Economic rent is the pure rent payable as a reward for utilising the productivity of land. It is derived by subtracting the elements like interest, wages, profits and depreciation from the gross rent or contract rent. To David Ricardo, it is surplus over costs or expenses of cultivation.

Question 5.What are Money wages?

Answer:

Money wages are the remuneration received by the labourer in the form of money for the physical and mental service rendered by him or her in the production process. Ex : If a labourer is paid ₹ 30/- per day. ₹ 30/- is the money wage.

Question 6.What are Real wages?

Answer:

Real wage is the purchasing power of money wages in terms of goods and services.

Question 7.What are Time wages?

Answer:

Time wage is the amount paid for labourers for a fixed period of work i.e., weakly, daily, monthly etc.

Question 8.

What are Piece wages?

Answer:

Piece wage is the amount paid for labourers according to volume of work, done by them.

Question 9.

What is Gross interest?

Answer:

The payment which the lender receives from the borrower excluding the principal is gross interest. Gross interest = Net interest + [Reward for risk taking + Reward for Inconvenience + Reward for management]

Question 10.What is Net interest?

Answer:

Net interest is the reward for the service of the capital loan. Ex : Net interest paid on government bonds and government loans.

Question 11.What is Gross profit?

Answer:

Gross profit is considered as a difference between total revenue and cost of production. Gross profit = Net profit + [Implicit rent + Implicit wage + Implicit interest + Depreciation charges + Insurance premium]

Question 12.What is Net profit ? [Mar. ’16]

Answer:

Net profit is the reward paid for the organizer’s entrepreneurial skills. Net profit = Gross profit – [Implicit rent + Implicit wage + Implicit interest + Depreciation charges + Insurance premium]

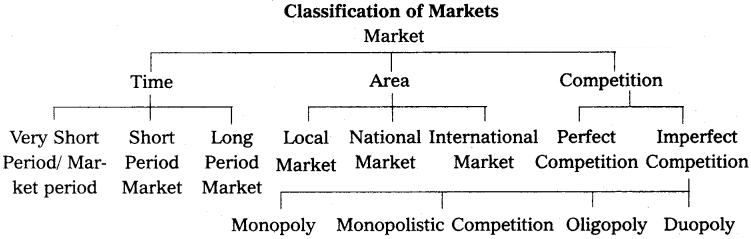

Question 1.Describe the classification of markets?

Answer:

Edwards defined “Market as a mechanism by which buyers and sellers are brought together”. Hence, market means where selling and buying transactions take place. The classification of markets is based on three factors. 1.On the basis of area 2.On the basis of time 3.On the basis of competition.

I. On the Basis of Area : According to the area, markets can be of three types. 1) Local Market : When a commodity is sold at particular locality. It is called a local market. Ex : Vegetables, flowers, fruits etc. 2) National Market : When a commodity is demanded and supplied throughout the country is called national market. Ex : Wheat, rice etc. 3) International Market : When a commodity is demanded and supplied all over the world is called international market. Ex : Gold, silver etc.

II. On the Basis of Time : It can be further classified into three types. 1) Market Period or Very Short Period : In this period where producer cannot make any changes in supply of a commodity. Here, supply remains constant. Ex: Perishable goods. 2) Short Period : In this period supply can be changed to some extent by changing the variable factors of production. 3) Long Period : In this period supply can be adjusted in accordance with change in demand. In long run all factors will become variable.

III. On the Basis of Competition : This can be classified into two types. 1) Perfect Market : A perfect market is one in which the number of buyers and sellers is very large, all engaged in buying and selling a homogeneous products without any restrictions. 2) Imperfect Market : In this market, competition is imperfect among the buyers and sellers. These markets are divided into 1. Monopoly 2. Duopoly 3. Oligopoly 4. Monopolistic competition.

Question 2.What are the characteristic features of perfect competition?

Answer:

Perfect competitive market is one in which the number of buyers and sellers is very large, all engaged in buying and selling a homogeneous products without any restrictions.

The following are the features of perfect competition :

1) Large Number of Buyers and Sellers : Under perfect competition, the number of buyers and sellers is large. The share of each seller and buyer in total supply or total demand is small. So, no buyer and seller cannot influence the price. The price is determined only by demand and supply. Thus, the firm is price taker. 2) Homogeneous Product : The commodities produced by all the firms of an industry are homogeneous or identical. The cross elasticity of products of sellers is infinite. As a result, single price will rule in the industry. 3) Free Entry and Exit : In this competition there is a freedom of free entry and exit. If existing firms are getting profits new firms enter into the market. But when a firm gets losses, it would leave the market. 4) Perfect Mobility of Factors of Production : Under perfect competition the factors of production are freely mobile between the firms. This is useful for free entry and exit of firms. 5) Absence of Transport Cost : There are no transport cost. Due to this, price of the commodity will be the same throughout the market. 6) Perfect Knowledge of the Economy : All the buyers and sellers have full information regarding the prevailing and future prices and availability of the commodity. Information regarding market conditions is also available.

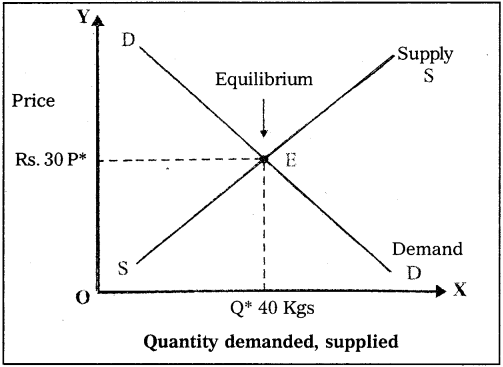

Question 3.Explain the meaning of perfect competition. Illustrate the mechanism of price determination under perfect competition. [Mar. ’17, ’16]

Answer:

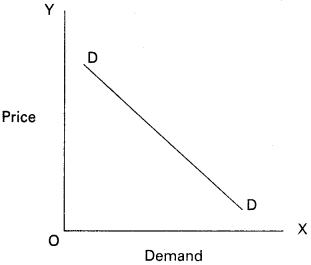

Perfect Competition : Perfect competition is a market sructure characterized by a complete absence of rivalry among the individual firms. Thus, perfect competition in economic theory has a meaning diametrically opposite to the everyday use of this term. In practice, businessmen use the word competition as synonymous to rivalry. In the theory, perfect competition implies no rivalry among firms. Perfect competition may be defined as that market situation, in which there are large number of firms producing homogeneous product, there is free entry and free exit, perfect knowledge on the part of buyer, perfect mobility of factors of production and no transportation cost at all. Price Determination under Perfect Competition : Under perfect competition, sellers and buyers cannot decide the price, Industry decides the price of the good. Market brings about a balance between the commodities that come for sale and those demanded by consumers. It means, the forces of supply and demand determine the price of the good. The following schedule and diagram help us to understand changes in supply, demand and equilibrium price.

Demand and Supply Schedule

Price (In Rupees)

Quantity supplied(in KGs)

Quantity Demanded (in KGs)

10

20

60

20

30

50

30

40

40

40

50

30

50

60

20

The above table shows the demand and supply schedules of a good. Changes in price always lead to change in supply and demand. As price increases, there is a fall in the quantity demanded. It means, price and quantity demanded have a negative relationship. At the sametime, if price of a commodity increases there is an increase in the quantity supplied. Therefore, the relation between price and supply of goods is positive. It can be observed from the table that when the price is ₹ 10/-, market demand is 60 kgs and supply is 20 kgs.

When the price increases to ₹ 20/-, the supply increases to 30 kgs and demand falls to 50kgs. If the price increases to ₹ 50/-, the supply increases to 60 kgs and demand is only 20 kgs. When the demand is less, price tends to decrease towards equilibrium price. When the price is ₹ 30/-, the demand and supply are equal to 40 kgs. This price is called equilibrium price which is ₹ 30, and equilibrium output and demand is 40 kgs. This process is explained with, the help of figure.

In the figure, the demand and supply of a commodity are shown on OX axis and the price of the commodity on OY axis. As per the diagram, the equilibrium price is found at a point where both demand and supply curves intersect each other at point E, i.e., OP price is the equilibrium price and OQ quantity is the equilibrium supply and demand.

Question 4.Explain equilibrium of the firm in the shortrun and longrun under perfect competition?

Answer:

Perfect competition is a market structure characterized by a complete absence of rivalry among the individual firms. Thus, perfect competition in economic theory has a meaning diametrically opposite to the everyday use of this term. In practice, businessmen use the word competiton as synonymous to rivalry. In theory, perfect competition implies no rivalry among firms. Perfect competition may be defined as that market situation, in which there are large number of firms producing homogeneous product, there is free entry and free exit, perfect knowledge on the part of buyer, perfect mobility of factors of production and no transportation cost at all.

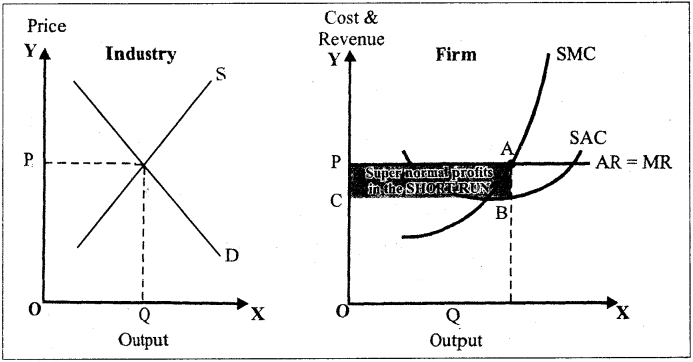

Equilibrium of a Firm : We have learnt that the price of a commodity is determined by the market demand and market supply under perfect competition. An increase in price of a product acts as an incentive in increasing production. As a firm aims at maximizing profit, it chooses that output which maximizes its profits. When the firm is in equilibrium, it has no desire to change its output.

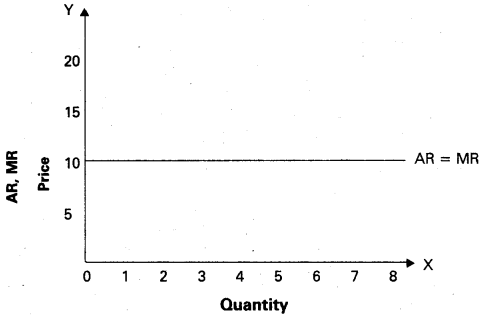

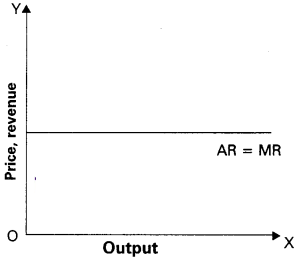

Equilibrium output is explained with the help of cost and revenue curves of a firm. In perfect competition, average and marginal cost curves are ‘U’ shaped one and average revenue and marginal revenue curves are parallel to OX axis. Since AR = MR, both these curves will merge into a single line.

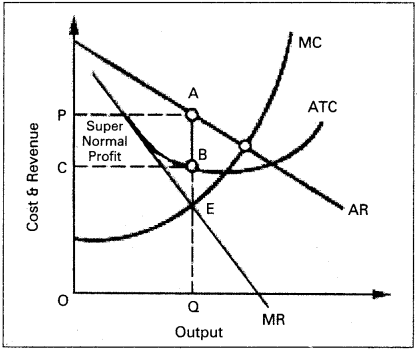

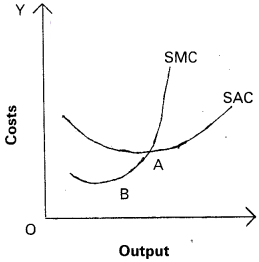

1) Short Period Equilibrium : Firms are in business to maximize profits. During short period, a firm cannot change fixed factors like machinery, buildings etc. However, it produces more output by increasing variable factors. Equilibrium output is produced in the short period where short period marginal cost (SMC) is equal to short period marginal revenue (SMR). The firm will be in equilibrium, when marginal cost curve cuts marginal revenue curve from below. During short period, a firm may get super normal, normal profits or losses. Two conditions are necessary for firm’s equilibrium. They are : i) MC = MR and ii) MC curve should cut MR curve from below. The figure shows the firm’s short period equilibrium.

In the figure quantity demanded and supplied are shown on OX axis and price of the commodity on OY axis. The diagram shows that the equilibrium price OP is determined by the industry at point E where the industry demand is equal to industry supply. The price, so, determined by the industry is passed on to the firm. This is shown by the horizontal demand curve of the firm. This line is also known as the price line. Since, competition is perfect, the AR curve (demand curve) of the firm is also the MR curve of the firm. The firm’s SAC curve and SMC curve are also shown respectively.

The profits of the firm are maximum at the output where MC = MR, that is, at output OQ, SMC = MR. At any output than OQ, MR exceeds MC, which would mean that if the production is more its profits will increase. At any output more than OQ, MR becomes less than MC, which would mean a loss to the firm. Thus, OQ is output of maximum profits. At the equilibrium point ‘E’, the price is equal to OP or AQ, while AC per unit equals QB, profit per unit is equal to B. Total supernormal profits will be equal to PABC, i.e., BA x OQ.

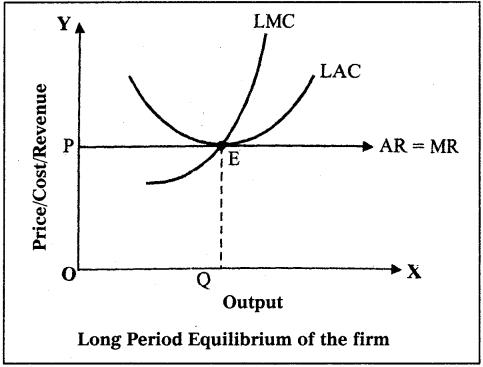

2) Long Period Equilibrium : We have seen that under short period, a firm can adjust its output, within limits, by varying the factors of production. But in the long period the firm can adjust its output to any extent because it can vary all the factors of production. Thus, it is certain that the firm will not incur losses in the long period. In the long period, the free entry of the new firms into the industry will wipe out the supernormal profits of the firm. Hence, in the long period, the frim wil be at optimum size where there is no profit – no loss. Firm gets only normal profits which are included in the long period average cost. In other words, under perfect competition, the individual firm at equilibrium earns normal profits only.

Therefore, AR = MR = LAC = LMC The figure illustrates the long period equilibrium of the firm. The quantity of a good is depicted on OX axis and price, costs and revenues are on OY axis in the diagram.

The point of equilibrium will be established at which the firm’s MR curve touches its LAC curve at its minimum point. At this point LMC = LAC. Thus, when a firm is in long period equilibrium the following conditions exist: At point E; P = AR = MR = LMC = LAC.

Question 5.What is monopoly? Explain how price is determined under monopoly?

Answer:

Monopoly is one of the market in the imperfect competition. The word ‘Mono’ means I ‘single’ and ‘Poly’ means ‘seller’. Thus, monopoly means single seller market. In the words of Bilas, “Monopoly is represented by a market situation in which there is a single seller of a product for which there are no close substitutes, this single seller is unaffected by and does not affect, the prices and outputs of other products sold in the economy”. Monopoly exists under the following conditions : 1) There is a single seller of product. 2) There are no close substitutes. 3) Strong barriers to entry into the industry exist.

Features of Monopoly:

1.There is no single seller in the market. 2.No close substitutes. 3.There is no difference between firm and industry. 4.The monopolist either fix the price or output.

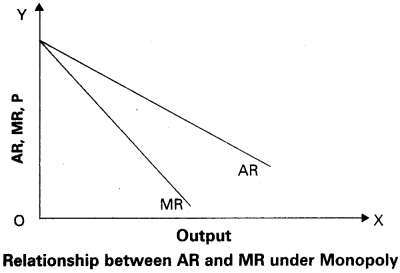

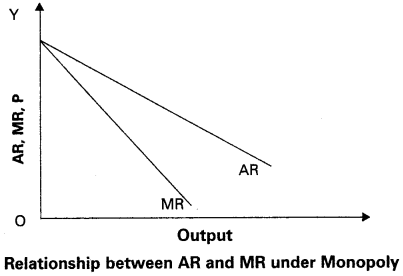

Price Determination : Under monopoly, the monopolist has complete control over the supply of the product. He is price maker who can set the price to attain maximum profit. But he cannot do both things simultaneously. Either he can fix the price and leave the output to be determined by consumer demand at a particular price. Or he can fix the output to be produced and leave the price to be determined by the consumer demand for his product. This can be shown in the diagram.

In the above diagram, on ‘OX’ axis measures output and ‘OY axis measures cost. AR is Average Revenue curve, AC is Average Cost curve. In the above diagram, at point E where MC = MR at that point the monopolist determines the output. Price is determined where this output line touches the AR line. In the above diagram for producing OQ quantity cost of production is OCBQ and revenue is OPAQ. Profit = Revenue – Cost = PACB shaded area is profit under monopoly.

Short Answer Questions

Question 1.Write a note on classification of markets based on time and area?

Answer:

Edwards defined, “Market as a mechanism by which buyers and sellers are brought together”. Hence, market means where selling and buying transactions take place. The classification of markets is based on three factors.

1.On the basis of area 2.On the basis of time 3.On the basis of competition. I. On the Basis of Area : According to the area, markets can be of three types. 1) Local Market : When a commodity is sold at particular locality, it is called a local market. Ex : Vegetables, flowers, fruits etc. 2) National Market : When a commodity is demanded and supplied throughout the country is called national market. Ex : Wheat, rice etc. 3) International Market : When a commodity is demanded and supplied all over the world is cdlled international market. Ex : Gold, silver etc. II. On the Basis of Time : It can be further classified into three types. 1) Market Period or Very Short Period : In this period where producer cannot make any changes in supply of a commodity. Here supply remains constant. Ex: Perishable goods. 2) Short Period : In this period supply can be changed to some extent by changing the variable factors of production. 3) Long Period : In this period supply can be adjusted in according to change in demand. In long run all factors will become variable. III. On the Basis of Competition : This can be classified into two types. 1) Perfect market : A perfect market is one in which the number of buyers and sellers is very large, all engaged in buying and selling a homogeneous products without any restrictions. 2) Imperfect Market : In this market, competition is imperfect among the buyers and sellers. These markets are divided into 1. Monopoly 2. Duopoly 3. Oligopoly 4. Monopolistic competition.

Question 2.Explain the equilibrium of the firm in the Short-run under perfect competition?

Answer:

Short Period Equilibrium : Firms are in business to maximize profits. During short period, a firm cannot change fixed factors like machinery, buildings etc. However, it produces more output by increasing variable factors. Equilibrium output is produced in the short period where short period marginal cost (SMC) is equal to short period marginal revenue (SMR). The firm will be in equilibrium, when marginal cost curve cuts marginal revenue curve from below. During short period, a firm may get super normal, normal profits or losses. Two conditions are necessary for firm’s equilibrium. They are : i) MC = MR and ii) MC curve should cut MR curve from below. The figure shows the firm’s short period equilibrium.

In the figure quantity demanded and supplied are shown on OX axis and price of the commodity on OY axis. The diagram shows that the equilibrium price OP is determined by the industry at point E where the industry demand is equal to industry supply. The price, so, determined by the industry is passed on to the firm. This is shown by the horizontal demand curve of the firm. This line is also known as the price line. Since, competition is perfect, the AR curve (demand curve) of the firm is also the MR curve of the firm.

The firm’s SAC curve and SMC curve are also shown respectively. The profits of the firm are maximum at the output where MC = MR, that is, at output OQ, SMC = MR. At any output than OQ, MR exceeds MC, which would mean that if the production is more its profits will increase. At any output more than OQ, MR becomes less than MC, which would mean a loss to the firm. Thus, OQ is output of maximum profits. At the equilibrium point ‘E’, the price is equal to OP or AQ, while AC per unit equals QB, profit per unit is equal to B. Total supernormal profits will be equal to PABC, i.e., BA x OQ.

Question 3.Explain the equilibrium of the firm in the Longrun under perfect competition?

Answer:

Long Period Equilibrium : We have seen that under short period, a firm can adjust its output, within limits, by varying the factors of production. But in the long period the firm can adjust its output to any extent because it can vary all the factors of production. Thus, it is certain that the firm will not incur losses in the long period. In the long period, the free entry of the new firms into the industry will wipe out the supernormal profits of the firm.

Hence, in the long period, the frim wil be at optimum size where there is no profit – no loss. Firm gets only normal profits which are included in the long period average cost. In other words, under perfect competition, the individual firm at equilibrium earns normal profits only. Therefore, AR = MR = LAC = LMC The figure illustrates the long period equilibrium of the firm. The quantity of a good is depicted on OX axis and price, costs and revenues are on OY axis in the diagram. The point of equilibrium will be established at which the firm’s MR curve touches its LAC curve at its minimum point.

At this point LMC = LAC. Thus, when a firm is in long period equilibrium the following conditions exist: At point E; P = AR = MR = LMC = LAC.

Quedtion 4.What is monopoly? What are its characteristics?

Answer:

Monopoly is totally a different market situtation compared with perfect competition. The word ‘mono‘ means single, and ‘poly’ means seller. Monopoly is said to exist when one firm is the sole producer of a product which has no close substitutes. In the words of Bilas, “Monopoly is represented by a market situation in which there is a single seller of a product for which there are no close substitutes, this single seller is unaffected by and does not affect the prices and outputs of other products sold in the economy”.

Characteritics of Monopoly: a) A single firm produces the good in the market. b) No close substitutes to this good. c) Strong barriers exist for the entry of new firms into the market. d) Industry and firm is one and same. e) Producer can control either price or quantity of the good. But he / she cannot determine both price and quantity of the good simultaneously.

Equilibrium and Price Determination under Monopoly : Price, output and profits under monopoly are determined by the forces of demand and supply. The monopolist will have complete control over the supply of the product. He also possesses the power to set the price to attain maximum profit. However, he cannot do both the things simultaneously, Either he can fix the price and leave the output to be determined by the consumer demand at this price or he can fix the output to be produced and leave the price to be determined by the consumer demand for his product.

Question 5.What are the characteristics of monopolistic competition?

Answer:

It is a market with many sellers for a product but the products are different in certain respects. It is mid way of monopoly and perfect competition. Prof. E.H. Chamberlin and Mrs. Joan Robinson pioneered this market analysis.

Characteristics of Monopolistic Competition :

1) Relatively Small Number of Firms : The number of firms in this market are less than that of perfect competition. No one can control the output in the market as a result of high competition. 2) Product Differentiation : One of the features of monopolistic competition is product differentiation. It takes the form of brand names, trade marks etc. Its cross elasticity of demand is very high. 3) Entry and Exit : Entry into the industry is unrestricted. New firms are able to commence production of very close substitutes for the existing brands of the product. 4) Selling Cost : Advertisement or sales promotion technique is the important feature of Monopolistic competition. Such costs are called selling costs. 5) More Elastic Demand : Under this competition the demand curve slopes downwards from left to the right. It is highly elastic.

Question 6.What is oligopoly? Explain its characteristics?

Answer:

The term ‘Oligopoly’ is derived from two Greek word “Oligoi” meaning a few and “Pollein” means to sell. Oligopoly refers to a market situation in which the number of sellers dealing in a homogeneous or differentiated product is small. It is called competition among the few. The main features of oligopoly are the following.

1.Few sellers of the product. 2.There is interdependence in the determination of price. 3.Presence of monopoly power. 4.There is existence of price rigidity. 5.There is excessive selling cost or advertisement cost.

Question 7.Explain the concept of duopoly and its characteristics?

Answer: